Wealthy vs Poor Mindset - (Part 3)

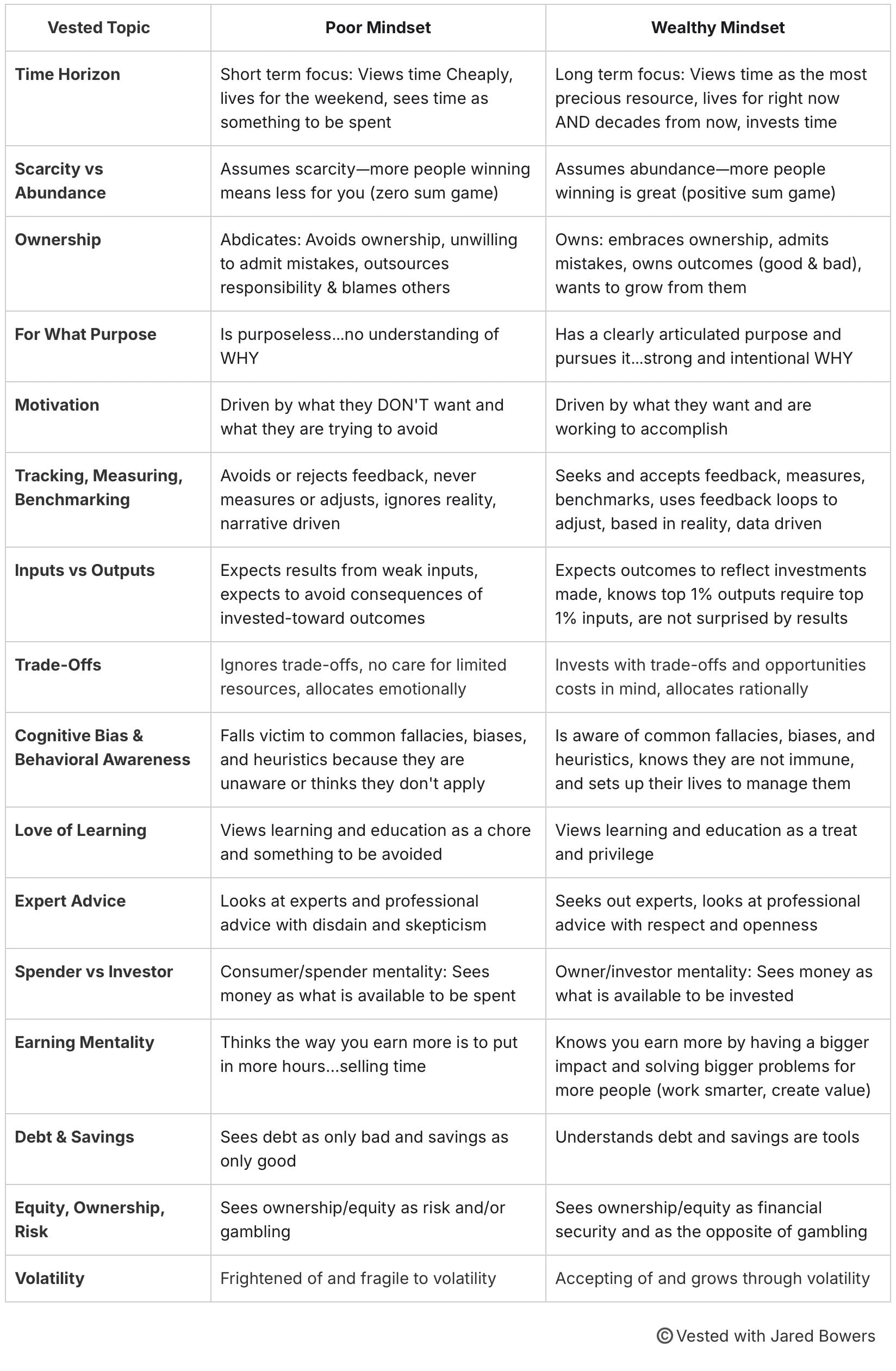

Full Wealth vs Poor Mindset Ledger

Synopsis

Episode 006: Wealthy Mindset vs. Poor Mindset (Part 3)

Synopsis In the final installment of the "Wealthy vs. Poor Mindset" series, Jared completes the 16-parallel ledger by focusing on Expert Advice, Earning Mentalities, Debt, Equity, and Volatility. This episode moves from high-level philosophy into the "dollars and cents" of how these mindsets manifest in our financial and professional behaviors. Jared challenges the common belief that debt is a moral evil, explains why income is a "value problem" rather than a "time problem," and shares a startling realization: the "Poor Mindset" is essentially a state of prolonged immaturity. By the end of this episode, you will have a complete diagnostic tool to audit your life portfolio and a roadmap for shifting your "batting average" toward the wealthy side of the ledger.

Detailed Sequential Outline

I. Introduction: Completing the 16 Parallels

- (0:10) The final six items on the ledger. This series is foundational because these mindsets interweave every concept discussed on the Vested platform.

II. Parallel #11: Expert Advice (Skeptical vs. Seeking)

- (1:11) The Poor Side: Views experts as threats with ulterior motives. Prioritizes personal anecdote over earned expertise. This skepticism keeps the individual "stuck" because they refuse to learn from those who have already solved their problems.

- (2:00) The "Advice Test": In groups, people assume those who struggle with money are most likely to listen to advice. In reality, the opposite is true. Long-term poor individuals are often the most skeptical.

- (3:15) The Wealthy Side: Already successful people are typically the ones most willing to pay for expertise. They view advice as a way to buy back time and accelerate results.

- (6:30) Application Across Life:

- Career: High achievers seek mentors; those who stay stuck resist them.

- Marriage: Strong couples seek counseling proactively to iterate toward excellence.

- Health: The fittest athletes have the most coaches.

- (8:30) Affirmation vs. Counsel: People in a poor mindset often seek sympathy (talking to others who are failing) rather than counsel (talking to those who have succeeded).

III. Parallel #12: Spender vs. Investor (Pleasure vs. Returns)

- (9:50) The Spender Mentality: Resources are for spending. Optimizes for immediate pleasure, comfort, and "the nice feeling of a purchase." Money "disappears" because it lacks a job.

- (11:00) The Investor Mentality: Resources are for investing. Optimizes for long-term ownership and impact. Delaying gratification isn't about deprivation, but about accomplishing a specific goal.

- (11:45) Every Dollar Has a Job: If you don't assign your resources (time, energy, money) a task, they "grow legs and walk away."

IV. Parallel #13: Earning Mentality (Time vs. Value)

- (12:56) The Poor Side: Views income as a function of Time x Rate. Sees income as fixed, capped, and externally controlled. "I need more hours for a bigger paycheck."

- (13:46) The Wealthy Side: Views income as a function of Value and Impact. Income is a "value opportunity." You earn more by solving bigger problems for more people.

- (14:50) Decoupling from the Clock: Approach your career acting as though your income is uncapped. Seek out responsibility rather than avoiding it; responsibility is the vehicle for adding value.

- (16:50) The Courage of Exposure: Transitioning to results-based pay feels vulnerable, but it is the only way to truly decouple time from earnings.

V. Parallel #14: Debt and Savings (Moral Categories vs. Functional Tools)

- (19:00) The Poor Side: Sees debt as a moral evil ("universal bad") and cash as a "universal good."

- (19:35) The Wealthy Side: Sees both as tools with specific uses. Debt is Leverage (a magnifier). It magnifies good outcomes when used well and bad outcomes when used poorly.

- (21:00) The Magnifier Analogy: Applying debt to a bad financial trajectory (credit cards, payday loans) accelerates the "bleeding." Applying the right debt (business expansion, right-sized mortgage) acts as an accelerator for wealth.

- (22:30) The "Idle" Risk of Savings: Cash has "termites" (inflation) eating it. A big pile of cash is useless until it is given a job to build or solve something.

VI. Parallel #15: Equity, Ownership, and Risk (Gambling vs. Security)

- (24:44) The Poor Side: Sees equity/stock market as "gambling." Prefers the illusion of safety in cash, not realizing that avoiding growth is the highest risk.

- (25:40) The Wealthy Side: Understands that ownership is the primary path to wealth.

- (26:50) The Two Markets: The market can be a gambling machine (short-term bets) or an ownership tool (holding great companies). The wealthy choose the latter. Sustainable wealth is built by owning things that create value, not just by trading price fluctuations.

VII. Parallel #16: Volatility (Danger vs. Price of Admission)

- (28:30) The Poor Side: Fragile to volatility. Interprets "ups and downs" as danger and retreats.

- (29:05) The Wealthy Side: Accepts volatility as the "price of growth."

- (30:30) The "Gift-Giving Mechanism": The market allows you to own the world’s greatest companies with the push of a button. The only "tax" is volatility. If you refuse to pay that price, you lose access to the benefits.

- (32:30) Life Volatility: Relationships and careers without volatility are often shallow or stagnant. Volatility is information, not necessarily risk.

VIII. Application: The Batting Average

- (34:50) Trajectory over Perfection: You don't need a "1000 batting average" (16/16) to be rich.

- 70% Wealthy Mindset: You are on a wealthy trajectory.

- Below 50%: This is a significant drag on all future returns.

- (36:30) Leaning into Discomfort: Pay attention to the points in this series that "stung" or made you defensive. That is where you are currently operating from a poor mindset.

IX. The "Childhood" Realization: Immaturity vs. Hopelessness

- (41:00) Kids as the Default Poor Mindset: Children naturally embody the poor mindset: short-term focus, scarcity, blaming others, skeptical of experts (parents/teachers), and surprised by cause-and-effect.

- (42:30) The Goal of Education: Maturity is the process of moving from the poor side of the ledger to the wealthy side. Falling on the poor side isn't a sign of being "stupid"; it is a sign of immaturity. You don't need to be "doomed," you just need to "grow up" in that specific area.

X. Closing Strategy: Practice and Outsourcing

- (45:45) Practice: Use the "Heck Yeah" approach to combat jealousy. Practice owning bad outcomes.

- (47:30) Outsourcing: If you have a "fatal flaw" in one area (e.g., behavioral discipline with money), outsource it to an expert. This is why professional portfolio managers exist—not just for analysis, but for behavioral strength.

Quotes to Remember

"The people on the poor side of the ledger—the ones struggling—are the ones who would benefit the most from expert advice, yet they are the least likely to listen."

"Slow and boring is often what results in the opportunity to have fast and exciting."

"Income is not a time problem; it is a value opportunity."

"Debt is wrong and bad when it is applied stupidly, but it is a powerful accelerator when used for the right purpose. It is a magnifier."

"Avoiding risk is not safety. What is risky is not pursuing growth at all."

"Volatility is the price of admission for growth. It is a tiny price to pay for the incredible benefits of ownership."

"Falling on the poor side of the ledger doesn't mean you're doomed or stupid. It means you are acting like a child in that area, and you need to grow up."

Next Episode: Transitioning from mindset to mechanics—diving into the core tool of the investor: The Investment Account.

Full Transcript

Introduction: Finishing the 16 Parallels

(0:16) Good day, investors. You are listening to vested with Jared Bowers. Welcome back to what is our third installment in our dive into the wealthy versus poor mindset.

(0:41) A three-parter already. Hey, I'm just as surprised as you are, but this is good news because we are setting the stage for nobody being surprised when I start throwing out five-parters by episode 10 and 10-parters shortly after that. Good news, right? The funny part for me is that you think I'm probably kidding. This is how sequels happen. Nobody plans it, but here we are.

(1:11) If you have not heard the previous two episodes on wealthy versus poor mindset, I'd encourage you to go back and listen to those, but you can also just dive right in right now, which is what we are going to do. Today, we are finishing the list, the last six parallels of the 16 items on the poor versus wealthy ledger. Then, after we get through those final six, we are going to close out our discussion on some encouragement and application of this whole wealthy versus poor mindset focus. So here we go.

Parallel #11: Expert Advice

(1:43) Number 11. Let's talk about mindset when it comes to advice, specifically expert advice. The poor mindset looks at experts and professional advice with skepticism, sometimes even with disdain or hostility. They see experts as threats, people with ulterior motives. They apply much more weight to anecdote than they do to real expertise, and because of that, the poor mindset side is much less likely to learn from and benefit from that expertise. But the contrast, on the wealthy side, those operating with a wealthy mindset seek out experts, and they respect that expertise that is earned, that is legitimate, not just claimed or anecdotal, and they leverage those experts and their expertise to accelerate their own results, to expand their own understanding, tying into learning that we just talked about in the past episode.

(3:04) They know that listening to experts in a field is a way to get something that is very valuable, not just good results, but they can save time and get better results in the process. I know I get these benefits when I listen to the experts that give me advice, and I see this rich versus poor parallel in a lot of the people that I help. If I could identify one test that determines the success that someone will have financially when I sit down to speak with them about their finances and their investments, it is their view of the advice that I'm bringing. Are they looking at it with skepticism or disdain, or are they looking at it with openness and willingness to learn and to listen?

The Humility of the Wealthy

(3:39) And sometimes I do this exercise with groups of people that I talk to. I ask the following question. When I am sitting across from someone to help them with their finances, who do you think is most likely to listen to my advice? And this is whether they're paying me or not. Is it someone who is not wealthy? Actually, let's make it more clear. Someone who is quite poor and has been for a long time. Or is it someone who is wealthy and has been wealthy for a long time? And I realize before I give the answer, I have certainly tainted this exercise for you, haven't I? You can guess what the answer is. It is the wealthy person based on how I've led us up to this point.

(4:34) But when I set this exercise up correctly, there are plenty of people who guess that it's the people who struggle with money that are more likely to listen to the advice that I give when I'm trying to help them. Because they're the ones that need it the most. But that is often, more often not the case. The people who are financially poor and have been for a long time, which means that they've practiced being poor, often through the application of poor mindset practices, tend to be the most skeptical of my advice and my help. And it's not just about me, at least I don't think it is. I've seen evidence of that mindset when it comes to expertise in general. More skeptical, sometimes disdainful, less likely to implement it. Even more likely to suspect an expert of having ulterior motives.

Implementation and Success

(5:12) Contrast this with wealthy people that I work with. And this applies to most of my clients. They are already successful with money. You would think that if they're going to listen to somebody, they'll just listen to themselves. They've done it. They've built financial wealth. They've gotten there, right? They figured it out. But that is not the case. Many of them, I would say most of them, are very humble when it comes to money. They have developed a practice of listening to experts in general, seeking out advice, wanting to learn from someone who does it professionally. And they are willing to pay money for it. You'd think that the people that I'm going to charge for my advice would be more skeptical of what I have to say compared to the people I'm trying to help for free.

(6:05) And in general, again, that is not the case. The expertise that I bring and the fact that other people are willing to pay for my advice signals something important to them. Money is my field of expertise. I am proven in it. What I say brings value. The decisions that I make on behalf of others when it comes to money and how I invest it have generally been positive. And I say generally because that's not the case with every investment decision that I make, every company that I buy, or every year of returns. But I have an established track record. I have expertise that brings value to my clients.

(6:45) And therefore, they want to listen to me and implement what I have to say. Because most of these wealthy people, most of the time, got into the position they're in, in part, because they listened to expert advice and applied it along the way, in the area that they built their wealth in. They built their wealth in part on the advice and knowledge of others. They listened to experts. They took good advice and they implemented it. I'm probably saying something obvious here, but I'm going to say it anyway. That is education. Learning from people who have greater knowledge in a subject or field than you do. And would you look at that? Didn't we just talk about a love of learning versus the avoidance of learning in our last rich versus poor parallel of our last episode?

Mentorship and Marriage

(7:31) This applies well beyond financial advice. The people with the fastest career advancement typically seek out mentors. Those mentors, the good ones, are people who have proven themselves in a field and then want to teach it to others. Those who stay stuck are the ones who tend to avoid or resist mentorship and don't try to learn from others, even when it is offered to them. They prefer to just do it on their own, to figure it out. That can work. Many people take this approach and they do figure it out. But there are better ways. You can see this on display oftentimes when it comes to marriage.

(8:11) Many of the strongest marriages, the people that I look up to and want to emulate in my own relationship, proactively seek out marital advice themselves. Even counseling. Even when there is not a clear problem that needs to be resolved. Because they know the value that they can get from that. From talking to an expert and applying that advice to what they're doing. And those who don't, even if they want a relationship that looks nothing like what they currently have, will often not listen to anyone, expert or otherwise, when it comes to how they approach their relationships.

The Coaching Paradox in Health

(8:45) You also see this in health. People who are the fittest, the strongest, the best at their chosen athletic pursuit are the ones that have the most and the best professionals around them. Coaches. The best in the world work with private coaches in multiple aspects of their discipline. And that is an interesting paradox, isn't it? Who needs the coaching more? The person you see in the gym that is clearly fit and healthy and moves proficiently, maybe even expertly at what they do, or the person who is struggling. Struggling with their weight, struggling with their movement, struggling overall with their health. But it is more often that person in the second category avoids or pushes back or actively disdains expert advice. Not always, but more often.

(9:38) Sadly, in that area and in every other area of life that this is applied to, the people on the poor side of the ledger, the people who are struggling, are the ones who would benefit by far the most from experts and from listening to that expertise. But they are the who are least likely to do so. And often those people on the poor side of the ledger will avoid listening to people who have success in an area because they feel like the expert can't relate or like they're being judged. My wife was talking to a friend not long ago who was going through relationship challenge on the brink of divorce. And her friend was lamenting that she didn't have anybody to talk to because everyone else around her seemed like they had great marriages.

(10:24) And so they wouldn't be able to relate. They wouldn't understand. Unfortunately, her friend was not looking for help or for advice or for counsel in order to learn and hopefully get better. Her friend was looking for sympathy, which is fine. It's good. But mostly she was looking for affirmation because she didn't want to talk to people who had successful marriages. She wanted to talk to the ones who had failed or struggling marriages. But talking to the people who seem to have it figured out is probably exactly who that person who is struggling needs to talk to.

(11:00) If you want to get in shape, who should you talk to about it? The person who's struggling more than you or the fit person? If you want to make money, who should you talk to? The guy who's broke or the successful businessman? One of them is going to be able to relate to you. The other is going to be able to help you. Look on the wealthy side of the ledger for the answer.

Parallel #12: Spender vs. Investor

(11:18) And I think this is important to keep in mind. Experts don't just cost money. You are buying back your time and you are buying better results. And oftentimes those results can be had for free. Plenty of experts are happy to lend their advice to people who genuinely want to listen and genuinely want to learn. And that can be one of the best investments that you can make. Okay, let's move on to the next parallel. And these last five actually have more to do with money. Not exclusively, but the money examples will apply very directly.

(12:06) And I'm going to go through them in a bit more rapid fashion. At least that's my plan. And this next one on the list, number 12, is the spender versus investor mentality. The poor mindset sees money and resources as what are available to be spent. They prioritize immediate wants and they aim for comfort, convenience, and that nice feeling when you buy something. And with this approach, they are often left with not much, but an empty bank account at the end of the month. On the wealthy side, those that practice a wealthy mindset in this area see money and other resources as what is available to be invested. They prioritize long-term returns. They aim for ownership. They want to have an impact with their investment. Yes, they also spend their money, but even their spending is properly seen as an investment in the problems they're trying to solve.

(13:01) And because of that, they get something really powerful. Compounding. I often summarize or describe this as the spender versus investor mentality. And this mindset definitely shows up in how we use money, but it also shows up in how we use our time and our energy. Because we know money is not the only currency that we invest. And it is probably the least valuable of the currencies that we invest. And this mentality between spender and investor, if you're on the poor side of the ledger, those people optimize for pleasure now. They spend emotionally and impulsively. They think that money just goes places. It disappears. Because they don't have a purpose for it.

(13:41) And it does disappear, to be fair. When you don't have a purpose for your money, when you don't give it a job, it does just find places to go. And this is also true for our time and our energy. I joke with my investment students that they need to assign every dollar a job. Because if they don't, those unassigned dollars will grow legs and walk away. Sometimes run away. And who the heck knows where it went once it's all gone. Those people on the poor side of the ledger believe that they'll make investments later. That they should be making now. They avoid building anything with their resources because it's slow and it's boring a lot of the time. They want immediate gratification right now. Not understanding that slow and boring is often what results in the opportunity to have fast and exciting.

(14:32) And that opportunity comes when it's been properly invested. And when it's been given enough time to grow. And that is the wealthy side. The investor mindset. The wealthy side of the ledger optimizes for long-term returns and results. Those people intentionally allocate their resources and delay gratification. Not forever, but to accomplish their goal. They see money as a tool. Not as the point. Not as the objective to be striven for. Strived for? You get the point. They believe that every dollar should have a job. And they give those dollars jobs. They focus on building wealth before they build their lifestyle.

(15:25) And I'm confident, because you live in the same world that I do, that you can think of and you can see examples of this all around you. People living on both sides of this mindset. You yourself are very likely an example of this on one side or the other. Maybe not in an extreme, but because money is so easy to measure, it should be easy to measure which side of the ledger we fall on when it comes to this. Spender versus investor.

Parallel #13: Earning Mentality (Time vs. Value)

(15:51) Plenty more to talk about, but we are going to move on to number 13. And this is our mentality when it comes to earning money. How we earn. And this may be a new concept to many people. When I bring this up, many haven't thought about money and earning in this way. And if I step on any toes, know that I don't mean to. The poor mindset applied to our earning mentality believes that the way we earn more money is to work more hours or just work long enough to get a promotion. The poor mindset views earnings as a function of time spent at a given rate, and they see their income as more fixed and capped and externally controlled.

(16:34) If I want a bigger paycheck, then I need to work more hours or overtime or I need to get a second job or I need to wait for my promotion. If I want to get ahead financially, I need more hours multiplied by my hourly rate or I need a different job title. Versus the wealthy mindset understands that earning more and earning in general comes from increasing value, having a bigger impact, and leveraging and using your skills and that impact that you have. It doesn't simply just come from putting more hours through a set wage. People on the wealthy side of the ledger see income and earnings as expandable, growable, and mostly driven by the problems that we solve and the value that we bring, not simply the time that we put in.

(17:20) See, the poor mindset thinks that income is a time problem, but the wealthy mindset knows that income is a value problem. More accurately, a value opportunity. And this is not an hourly versus salary thing. Regardless of how you are paid, these two mindsets exist in both. You earn more by solving bigger problems for more people, not simply by working more hours or working long enough to get a promotion and a salary bump. And I believe that this is an important thing to say and to understand. You want to be in a position where you are trading the value that you bring for money, not just the time that you bring for money.

(18:07) You want to approach the jobs that you do in the career that you have, acting as though your income is uncapped and only limited by problems that you can solve. And in most cases, the opportunities for that are infinite. Rather than seeing your income as capped by the amount of time that you can put in or the number of years that you've worked. And you should want to seek out responsibility because of the added opportunity that it gives you to solve problems and bring real value, rather than the poor mindset side where they're simply just doing the calculation of hours put in.

(18:36) The poor mindset side typically wants to avoid responsibility because often the attitude is that's just more effort for the same pay. That's often how it's translated or seen. But we definitely want to focus more on outcomes, not on the clock. Now, some hearing this are going to think, all right, easy for you to say, Jared. You work in a job where that relationship exists as the default. And in a way you are right. It doesn't matter at the end of the day or the week exactly how many hours I put in. It matters how much value I bring. My job is one of those that can be perfectly aligned with this philosophy.

(19:16) If I add more value over time, I get paid more. If I destroy value or don't add value over time, I get paid less. So you may say that it's easy for me to say and that not every job is like that. And there is truth to that. But I believe and I would love to convince you that in every career, anyone can work themselves into a position or a job or create that job themselves where that relationship does exist. Where getting paid based on your results and the value that you produce is the default, not just for the time that you put in. Show incredible value in your work and see what happens.

(20:03) Whether you are in an entry-level hourly job or a mid-level salary job or any other combination, see what happens. They should promote you and value you based on the value that you bring. And if they don't, you will be in a great position to find another job that will, or create that job yourself. Show what kind of value you bring based on how you are investing your time and energy and expertise in that job. And every chance that you get, ask to be put in a position where you are compensated based on your output, based on your actual results, not just the time that you put in or how long you've been there.

(20:41) And this is not something that can happen overnight. And it does take a level of courage because you are exposed in that position. If you're working in a job where your pay is directly tied to your measurable results, that is exposing. That can feel vulnerable in some cases, but it is worth it. It is how you decouple the hours you put in from how much you get paid. And that is not so that you can work less. It is so that you can be paid based on the value that you bring. And it is something that has developed over years and decades in most cases, but it is so worthwhile to do that it must be pursued.

(21:22) And what I'm not going to get deep into now, but I am going to mention because it's very much related to this is the other way that we decouple our time from our earnings, which is investing our excess cash into appreciating assets, taking our cash flow and buying things with it that go up in value over time, get your money working for you. And you can and will make money regardless of the time and effort that you put in in the future. That is also incredibly powerful and it's how most wealthy people get and stay wealthy.

Parallel #14: Debt and Savings (Tools vs. Morality)

(22:03) There's a lot to talk about here and we will in the future, but we are going to pause on that for now because we're going to talk about another money-related theme, which is about debt and savings. And this is likely another topic that may be contrary, or different at least, to what a lot of people were raised to believe. And you may have very strong feelings when it comes to this one specifically. This next parallel, number 14, may surprise some people because the poor mindset sees debt as a universal bad and cash as a universal good. Maybe even more strongly than that, they see debt as evil. Cash is king and debt is danger, maybe even morally wrong.

(22:42) Contrast that with the wealthy mindset. Those people operating on the wealthy side do not see debt as good. They also do not see debt as inherently evil or bad. They understand it for what it is. It is a tool. And they see savings for what it is, also a tool, but a pretty weak one if it just sits there. It is an unused but high-potential asset that actually needs to be applied for it to have its best value. Both debt and savings must be used intentionally and allocated based on the purpose that they're trying to have, the outcomes that they're trying to get.

(23:13) And this mindset, yes it is about debt and savings, but it's really about the ability to evaluate cost, risk, and opportunity. Because the poor mindset sees things in moral categories that shouldn't be. Debt equals bad, savings equals good. But the wealthy mindset sees money as a system of tools and trade-offs that can and need be learned and then need to be applied appropriately in order to unlock value. A moral framework doesn't need to be applied when it comes to these tools that we have. The morality comes in based on how we apply these tools. Debt is wrong and bad and stupid when it is applied stupidly, when it is used poorly.

(24:07) But when it is used well for a specific purpose, for the right purpose, it is simply a tool that can be used as an accelerator and can help us achieve the results that we're going for. Effective purpose and proper use can make it a good tool when it is used well. Not good in the moral sense, good in the helpful sense. And those on the wealthy side understand that savings and cash are idle and effectively useless unless they are actually deployed. Savings does give us optionality, but that means that we need to actually pick an option.

(24:46) Because just to make sure we're on the same page, when I say savings, what I'm referring to is cash, uninvested money, money that is just sitting there, whether it's stuffed in a mattress or in a savings account at a bank, maybe earning a bit of interest but not invested or not spent solving worthwhile problems. And I'm not saying have no savings. An appropriate amount of savings is very smart. I'm talking about leaving too much of a high potential asset uninvested. And consider what I brought up earlier. Money needs a job. And if you don't give it one, at best it just does nothing. And at worst, it finds its own places to go.

(25:26) And even if you hold on to it, it has termites that eat at it called inflation. Now, I will note and state this clearly. There are good types of debt and bad types of debt. Again, not in the moral sense, but in the potentially helpful versus certainly unhelpful sense. Because thinking with the poor mindset that all debt is dangerous or bad or evil is just a misunderstanding of the tools that are available to us. Debt is leverage. That's a word that's commonly used with debt. And that means that it magnifies results. Think of the simple tool of a lever.

(26:11) It enables you to lift something that you otherwise couldn't lift. That is what I teach my students. Debt is a magnifier. And it will magnify good outcomes and it will magnify bad outcomes. And if you apply a magnifying tool to a bad money situation, which is how most people use debt, at least certain types of debt, credit card debt, department store debt, payday loans, buy now, pay later. For sure, using debt in those situations is going to make that situation worse. Because you are adding debt to an already bad trajectory. A situation where what you're buying you can't afford in the first place.

(26:48) Your financial trajectory is going to go more strongly in the wrong direction when debt is applied to it. And in general, debt is a bad thing for many of these people, probably the majority of people, of households, families, because when you look at their money situation, it's not stellar. We've talked about some of those stats before. And yes, applying more debt to a bad financial situation is going to make the outcomes worse. It magnifies what is there and the direction that they are heading. But if you are managing your business, your household, your career, with intention, with purpose, and you use tools at the appropriate times and in the appropriate ways, those tools can be helpful.

(27:35) Debt applied in those situations, at least the right kinds of debt, can magnify positive results. It can and will be an accelerator that is very powerful and will not add undue levels of risk because you've managed it well, because you are using it appropriately. A reasonable amount of school debt to get a valuable degree. A business loan to expand and take advantage of a market opportunity. A properly sized mortgage for your primary residence for your family. And going back to the cash and savings side of the discussion, let's talk about that a little bit more.

(28:08) The poor mentality sees a big pile of cash as a universal good and the thing that you should be striving for. But typically, those with a poor mindset want a big pile of cash so that they can have it to spend, which is not the same thing as being wealthy. On the wealthy side of the ledger, a big pile of cash is, as I said earlier, effectively useless until and unless it is given a proper job. To own something, to build something, to solve a problem. It could even be used to pay off that debt that is no longer serving its purpose or could be better applied elsewhere as an investment in appreciating assets.

(28:51) And you know what else it could be used for? To spend. Because we have expenses and we should spend our money, even on some fun and frivolous things. Let's just make sure that we spend it well. Debt is not universally bad and savings is not universally good. Applying a moral binary to a tool does not make sense. What matters is how it is used.

Parallel #15: Equity, Ownership, and Risk

(29:09) And this ties into our next rich versus poor parallel. Number 15. And this is about equity, ownership, and risk. The poor mindset sees ownership as risky or gambling and they fear equity ownership, oftentimes access through the stock market, because it feels uncertain. The wealthy mindset views and treats ownership as what it is, the path to financial security and the opposite of gambling. Let's dig deeper on the poor side. Those with a poor mindset in this area prefer the illusion of safety, which to them is cash. They avoid taking risks because they don't understand its purpose.

(29:57) And they would rather have safety and savings versus what they perceive as risk through owning something. And I hear the poor mindset applied frequently in this one phrase. "Oh, the stock market is just gambling." And that is a misunderstanding of how a tool is used versus how a tool is best applied and is meant to be used. Sound familiar? The stock market is a tool. It gives us the ability to use that tool in many different ways. Two primary ways, I would argue. And I will be the first to say that the primary way that the stock market is used by most people is as a gambling machine.

(30:38) Because most of the active market participants are taking short-term positions. They're making bets. They are not approaching the markets in the second way, the way that a wealthy investor-minded person approaches the market, which is with an ownership mentality. And the market gives you the ability to do either one. You can use it for gambling, but it is best applied and should be used as a tool to own great companies for a long time. Be a business owner and act like one, which means we care about the business in terms of how it is actually doing fundamentally, the value that it is creating for its customers, and the results and the revenue that it is bringing in and the profit that it is generating in that process.

(31:25) And this contrast of poor mindset versus wealthy mindset when it comes to equity and ownership and risk is very important in order to get the money and the life outcomes that we want. And the wealthy mindset, as it applies to this parallel, looking at equity ownership, understands ownership is the primary path to wealth. Those on the wealthy side understand that controlled risk is necessary. They embrace equity ownership as long-term security, not as short-term danger. They invest with a long-term business owner mentality. Most wealthy people got wealthy and get wealthy because they owned something that went up in value, often because they created that value themselves through starting a business, not just from a paycheck.

(32:09) Employment can definitely help. A big paycheck can certainly help. But real long-term sustainable wealth, in most cases, is built and kept through owning assets that go up in value over time. Ownership. Yes, ownership comes with uncertainty. It comes with risk. It comes with volatility, the ups and downs. And people with a poor mindset think that the safest place for their money is where nothing fluctuates. It's in cash or a CD or a savings account. Gold is often billed as this. We won't get into that now, although I have strong opinions. And don't get me wrong, ownership can be risky.

(32:47) It does come with downsides. But ownership is also rewarded. This is something to dig into more in the future, but avoiding risk is not safety. What is risky is not pursuing growth at all. That is where the biggest downside lies. If you don't own anything that can go up in value, your financial trajectory can't go up either. That, to me, is a much bigger risk than the ups and downs that you'll experience on an otherwise generally upward and to the right direction.

Parallel #16: Volatility (The Price of Growth)

(33:17) And that brings us to the 16th and final item on our list, volatility. Something that we've touched on and referenced in our discussions on equity and ownership and risk. And yes, this one ties into money pretty directly as well, but it also ties into many other areas of life and investing that we talk about and that we'll focus on. The poor mindset, as it is applied to volatility, is frightened of and fragile to volatility. Those with a poor mindset interpret fluctuations, the ups and downs, as danger. And they want stability at all costs. They want to avoid uncertainty.

(33:59) And that often translates into wanting progress without being willing to pay the cost of that progress. On the wealthy side, those with a wealthy mindset are accepting of and grow through volatility. They see fluctuations as information, as opportunity, not inherently as risk. Those with a wealthy mindset understand that progress requires ups and downs, and they lean into and grow from that volatility instead of retreating from it and avoiding it. The most successful embrace volatility because volatility is not the enemy. Volatility is the price that we pay for growth. It is the price of admission.

(34:36) And it is a price that is worth paying. Because if you want wealth through equity ownership, this very clearly applies to the stock market. You do not get there without the ups and downs. Volatility is the price that we pay. Something that I say often to my clients, my students, anybody that's willing to listen to me about the stock market, and if you are listening to me right now, I suppose that means you as well, is this. We get incredible benefits from the market. It is a wonderful, magical, gift-giving mechanism that we don't even have to make an application to participate in.

(35:10) We don't have to ask anybody's permission to invest in and to own some of the greatest companies in the world. We can do that for nothing more than just opening up a brokerage account, depositing some money into it, and pushing a few buttons on a computer. It is incredible. And the only cost that you have to pay, besides the opportunity cost of the cash that you're giving up to own it, is volatility. The ups and downs of the market. And that is a tiny, small price to pay for the incredible benefits that we can get. But with the wrong focus, and the wrong view, and the wrong understanding of volatility, that can really get us in trouble.

(35:54) Because volatility, those ups and downs, can cause us to make some bad decisions. We will talk in the future about those bad decisions, and what volatility can point us toward and cause us to do, tempt us to do at least. But as it relates to the poor versus wealthy mindset, volatility is seen only as a negative by those on the poor side of the ledger. Volatility is seen as necessary and part of the process, and part of the cost that we pay by those on the wealthy side of the ledger. And this is not just in the financial markets. That also applies to most things in life.

Volatility in Life Portfolios

(36:30) We don't make progress in relationships without volatility, ups and downs. Show me a relationship that has never had any volatility, any period of downs, any period where they've made big upside swings, and I will show you a very shallow relationship. Show me a career with no volatility whatsoever, and I will show you that they are an accountant. I'm kidding. I love accountants. I am good friends with many of them. I just like teasing them. But oftentimes, very likely, a career with no volatility is reflected in the impact and in the salary.

(37:04) And I will say, there are plenty of accountants that have fantastic impact, and they are reaping the rewards of the great work that they do and the effort that they put in and the volatility that they've had up to that point. Show me a successful athletic career that did not have significant volatility, ups and downs. Volatility to those with a poor mindset equals bad. Volatility to those with a wealthy mindset equals the necessary price that we pay for an opportunity that we get to take advantage of.

Series Wrap-Up: Conclusion and Application

(37:43) Okay, we got through all 16. And in doing so, we set the stage to be able to go further into many of the concepts that we're going to dive into related to everything is investing and all that we are going to dig into here invested. Because the poor versus wealthy mindset permeates all of it. We actually touched on a large percentage of the philosophy that makes up what we are going to dive into deeper from here. Because these 16 parallels of wealthy versus poor interweave so much of it.

(38:13) Every concept that we will talk about regarding money, life, and our investment in these areas has applications of the wealthy versus poor mindsets. And if we approach the world with a wealthy mindset, our outcomes are going to reflect that versus if we approach life and investing and all that we do with a poor mindset, our outcomes are going to reflect that as well. And I will say this again, where you fall or where you primarily fall on the poor side versus the wealthy side of the ledger likely has a lot to do with where you're at right now in terms of resources, money, relationships, health.

(38:48) But more important than that is our trajectory, the direction that we're going. Because the mindset that we into life and that we carry into our investments that we do or do not make determines what direction we're heading and the returns that we will be getting. And this is when I like to talk about our batting average. Because almost no one that I meet, even the most successful people that I know are batting 100 on the wealthy versus poor mindset. Wait, batting 1000? I am not a fan of baseball. I'm sorry. Maybe batting average is the wrong analogy for me to pick.

The Batting Average of Mindset

(39:24) I think it's batting 1000. But just to be safe, how about I talked about it in percentage terms to make sure that we're all on the same page and to make sure that I don't keep messing up this analogy. If you are hitting 70% or greater on the wealthy side, I'd say you're probably rich. And maybe it hasn't shown up yet in your investment accounts. But if you are hitting 70% or greater in these categories on the wealthy side, you are on a trajectory of building wealth in many areas of life.

(39:51) And I would say that if you're hitting less than 50% on the wealthy side, meaning that you are mostly landing on the poor side of the ledger in the majority of these cases that I talked through, that is going to result in a significant drag on your current and future returns across all areas of life that you care about and that you invest in. And people that are in that category, mostly falling on the poor side, are probably already poor in many of the areas that we talked about, and are most likely going to stay that way without changing their approach, without shifting those mindsets more to the wealthy side.

(40:29) And what I said in the past episodes on this topic, and maybe some of what I said today, stepped on some toes. Plenty of what I just talked through might even sting a little bit, because everyone falls on the poor side of the ledger in at least a few areas. And it is not fun to hear and to recognize that in ourselves. And I hope this is an encouragement. I have yet to meet a person who is 16 out of 16 on the wealthy side of the ledger. Perfect is not necessary for progress.

Awareness for the Sake of Improvement

(41:02) And what we talked through is introductory into many of these concepts. Some of these contrasts deserve their own deep dive, and I think that that's very likely going to happen in the future, certainly with some of them. There is a lot to unpack from here, and we will. But with what we've covered so far, here is what I would encourage you to do, especially as it relates to toes that may have been stepped on. Pay particular attention to what you had a negative response to. And if you did have a negative response, there was likely something that I said on that topic that you did not like.

(41:39) And I probably did at some point, hopefully many points, say something that created that warm fuzzy feeling that you get when you hear something that you already strongly agree with. We like hearing those things, said to us, that we already strongly believe. But that's the less important part. Not the unimportant part, but the less important part. What we don't like hearing, or what we have a negative response to, is what we need, is what you need to pay particularly close attention to.

(42:02) Because that is most likely where we can identify the areas that we struggle with, where we lean more on the poor side of the ledger. And if we can lean into that discomfort, that is a powerful tool to identify where we need to focus, where we may be driven more by a poor mindset versus a wealthy mindset. And I want to acknowledge, as I'm talking about stepping on toes and hearing things that we may want to push against, I am not in any way an example of a perfect batting average.

Jared's "Poor Mindset" Struggles

(42:33) When I say everyone struggles with things on the poor side, I really do mean it. I am part of those people. I am a member of the poor club on many days. When I say I know successful people that struggle with many of these on the poor side, that also applies to me. I can often be driven by what I don't want rather than what I do want. That is a violation of what I talked about when it comes to motivation. I have to catch myself because I can fall on the poor side of the ledger on that.

(43:07) I like to pretend, in many ways, in many of the things that I pursue in life that trade-offs don't exist. I do not acknowledge opportunity cost. I don't allocate rationally many times. I think that I can lift all the weights, cycle all the miles, and do just fine without pause for months or years at a time. I have tried that. I was wrong. My attention is split often too many different ways. My spotlight of attention has been pulled in too many different directions to the point that it has been dimmed at times.

(43:36) Again, on the trade-off side, I like to pretend that reality does not apply to me. With biases that we talked about in the episode, I like to think that I am so aware of the cognitive biases that I am immune to most of them, but I am not. Also, this is just one more example, not the final example, there's plenty of other areas that I struggle with as it relates to the poor versus wealthy mindset. I have a tendency to try to minimize volatility in my own life.

(44:02) Now, focusing on the appropriate amount of volatility makes sense. We do not want to try to maximize volatility in our lives, at least in most areas of life. We might know some people who try to do that. They're typically not the type of people we want to be around. But I tend to think, and I'm tempted to think, that because I'm experiencing volatility, ups and downs, that that represents a problem, an inherent problem on its own. And I often respond badly to that volatility. It makes me want to sell. It makes me want to pull back.

(44:43) But I need to listen to my own preaching. When I have volatility in a relationship, that's often because we're working on something meaningful together, and there's opportunity for growth. When I have volatility in my performance in the gym or on the bike, I hate that. I want consistency. Actually, I want consistent growth. But in order to get the ups, there also has to be some downs. And I do not do a good job of focusing on that and understanding that sometimes.

(45:20) I do that pretty well in my investment portfolios with money. When prices go down, I see it often as an opportunity to take advantage of. But in other areas of life, when it comes to volatility, I can really struggle, and I do struggle. Volatility in my relationships can throw me for a loop. Volatility in my health, I have very little tolerance for. Volatility in my schedule, I can act like a certifiable baby when it comes to a wrench being thrown into my perfectly laid plans.

The Childhood Connection

(45:53) So as I'm talking through poor versus wealthy, the contrasts, the trade-offs, I am trying to hear much of what I'm talking about, and I am feeling the sting of it myself in many directions. And you know, I think this is interesting. I've been working on and refining this wealthy versus poor mindset list framework for a couple years now. And interestingly, when my wife read through this most recent update, all 16 points, she told me that she has interactions with people who embody many, if not most, of these poor mindset traits on a daily basis in the volunteering that she does at our kid's school.

(46:18) And no, of course, it is not in the teachers. It's not in the parents, or at least not in most of the parents. It's not the administrators. The people who embody many of these poor traits are the little people, otherwise known as children, the kids. And that made a light bulb go on in my head. Lightning has just struck my brain. Because think about it. Most kids embody most of the traits of the poor mindset. We can see it clearly. They have a very short time horizon.

(46:53) They have a scarcity mentality when it comes to most things. You getting something means me getting less. They, by default, tend to blame others. You didn't remind me it was due. My mom didn't pack my lunch. I didn't do that. They are, many times, driven by avoidance. What they don't want versus what they actually do want. And they are constantly surprised about the cause and effect relationships of life. They shouldn't be surprised, but they are.

(47:24) They treat experts, often, and those experts in their life are their teachers, their parents, very skeptically, and are often loathe to take advice and instruction when they are given it. They take ownership of very little. Now, of course, this does not apply to all kids. But especially when you look at the younger grades, let's say kindergarteners, first, second graders, you can see these applied very directly. And it is not because they are dumb. It is not because they're bad kids. It is because they are children.

Immaturity vs. Hopelessness

(48:02) And they have a lot of learning to do. And we, as parents and teachers, have a lot of teaching to do. And schools, good schools, our school, hopefully many or most schools, are set up to train kids for the wealthy side of the ledger, in nearly every one of these cases that I pointed out. That poor mindset that kids exhibit doesn't mean that they're bad kids or that they're defective. It just means that they're immature. It means that they're children, and they need to be educated, and they need to grow up in the right environment, that will train them toward the wealthy side of the ledger.

(48:34) That is exactly what we're trying to do as parents and as teachers. And I say all this in the hope that this will be an encouragement. Because if you, like me, as I've just admitted, struggle with many of these areas, if you fall on the poor side of the ledger, that doesn't mean that you're doomed. It doesn't mean that you're stupid. It doesn't mean that you're going to always be pointed in the wrong direction. It means that we need to be educated, and we need to grow up. It is more of a sign of immaturity and less of a sign of hopelessness.

(49:04) Because it can be learned, and it can be practiced. And when I identify that I fall on the poor side of the ledger in one of these areas, if I am approaching it correctly, I try to recognize that as an area that I need to grow in. Maybe an area that I need to grow up in and stop acting like a child. And we are all prone to acting like children in different areas of our lives, aren't we? And those areas are very likely, almost certainly, the areas that we exhibit mindsets and approaches to life that fall on the poor side of the ledger.

The Practice of Shifting

(49:40) Now these last three episodes were more philosophical than practical and application-based. But I am confident that you are going to be able to get application from many of these things that we talked about. And as you're looking at your own ledger, awareness is the first step. But it is not the last step. We should look for ways to identify where we fall on the poor side of the ledger, and then actively practice shifting our mindset away from the poor side and toward the wealthy side. And that is the operative word, practice.

(50:15) It is a practice and it needs to be deliberate. When we identify an area or multiple areas of struggle where we may fall on that poor side, we need to actively and purposefully practice the other side, the wealthy mindset. When it comes to something like scarcity versus abundance, when that jealous feeling arises, we need to actively practice saying, good for them, I hope they're even more successful. That heck yeah approach. When we make mistakes, we need to see it as an opportunity to learn, not as a red mark on a record or an excuse to avoid learning or avoid being a beginner.

(50:53) If we are bad at time management, wasting our time, our most precious resource, we need to try to shift our focus to identify how we can invest that time better and not just spend it. We need to practice ownership, not just of equity with our money. We need to practice owning outcomes, both good and bad. And when we are involved in something that goes poorly, we need to own that. And the great thing about that is when we're involved in outcomes that are going well, if we have successes, we can and should practice owning those as well.

(51:26) It goes both ways. When we are presented with an opportunity to learn in a situation where we are clearly not an expert, maybe we are quite ignorant by contrast, we need to practice embracing that, embracing the discomfort of being a beginner, because that is how we start. And that's how we move toward proficiency. The only path to getting better at anything that can resemble expertise. And when we encounter volatility in our life, we need to recognize it as a cost that is required for the progress that we are trying to make.

Superpowers and Fatal Flaws

(52:01) And as an opportunity to learn and to make adjustments, not just something that needs to be pushed against or avoided or complained about. If we actively practice these things, and over time, we will get deeper into how we can apply these frameworks, practices, pursuits around how we develop skills on the wealthy side of the ledger, we can shift our default state. We can increase our batting average. Batting a thousand is not required for success. And as I say that out loud, I realize, yes, it is batting a thousand.

(52:32) Got it figured out. When you look at the most successful people who are among us, you can often trace that success to being really deep and locked in, in a few of the items on the wealthy side of the ledger, and avoiding most of the negative side. Those are superpowers, truly. And again, that success can be traced to those superpowers. Not necessarily crushing it on every single one of the wealthy category, in all 16, probably just a few, but they are so strong in those few that they result in incredible success.

(53:09) And the reverse is often also true. When you see someone who is struggling mightily, living poorly in their life, not just with money, but in other areas also, it often isn't the result of being on the wrong side of the ledger and everything. It's often being on the poor side in the majority of things, or enough of the things where they are really, really deeply on the wrong side, going in the wrong direction. Instead of superpowers, these would be fatal flaws. And it is very hard to overcome fatal flaws, even with really strong application on the wealthy side in other areas.

(53:49) If you are an expert practitioner on the wrong side of the equation, those returns that you're getting can be quite large. But when it's in the negative direction, such as when we practice our fatal flaws, it almost doesn't matter where we fall on the wealthy side, in those other categories. Strong negative returns in just a few of the categories can be very difficult to overcome, even if you are good or even excellent at investing on the other side.

The Strategy of Outsourcing

(54:14) And for the areas that we struggle, it is a practice of mindset. We can also consider outsourcing some of those things. It doesn't apply or work in every category. And I am a big believer in DIY, do it yourself. But sometimes the best thing that we can do is give the reins to someone else and just follow their instruction, follow their lead. A great example of this is with money management. I'll talk more in the future about the importance of owning your money, and not just assuming that the best way to get good results is to hire a financial advisor.

(54:59) But my job as a portfolio manager for the wealthy exists because my clients want to outsource it to someone who is an expert at it. And I better do a good job of it. They're paying me money to do it. And what makes me good at it is less about finding the right companies to invest in, that is important, but it's actually more about the tools and rules and strategies. Lots of people could find and build portfolios of quality companies that will perform well. But I believe my greatest strength is actually on the behavioral side of managing and investing money.

(55:27) In addition to the strength of the analytical side, identifying good investments, and my clients, even though they're quite good at managing money on their own, they have outsourced that management to me. Other examples where outsourcing might be a good strategy for overcoming our tendency to be pulled in the poor direction could be with our physical health, or our food and nutrition, our workouts and getting and staying in shape. We might just need to default to the experts and listen to them, not just think that we can manage it on our own.

Foundations of Vested

(55:54) Again, outsourcing is not going to apply for everyone everywhere. Most of what we do needs to be owned fully by us. But outsourcing is and can be a useful tool. It's a strategy. And we'll talk more about those strategies in depth another time. Consider the ledger, the poor versus wealthy side of the ledger, and look for ways to identify which side you are on, which side you operate on. I am glad you've taken the time to walk through all 16 of these parallels with me, because they permeate and weave through every concept that we are going to talk about from here.

(56:38) And that is why this three-part mini-series, this early in our podcast journey, happened. Because it is foundational. And as a reminder, you can find a list of all 16 of the poor versus wealthy traits on the website, vestedjb.com. And I am looking forward to going deeper from here. Okay, thank you for investing in yourself and in those around you. I will talk to you next time.

(57:18) I think just this week alone, I have been on the poor side of the ledger in almost every category. Maybe I am batting 100.

(57:29) [End of Transcript]